Instant CRE insight

BUILT FOR COMMERCIAL LENDERS

Every CRE banker knows the questions — Is the NOI real? Who are the tenants?

Can this loan refinance

itself? We built a platform around those exact questions, so your team gets answers without the manual

work.

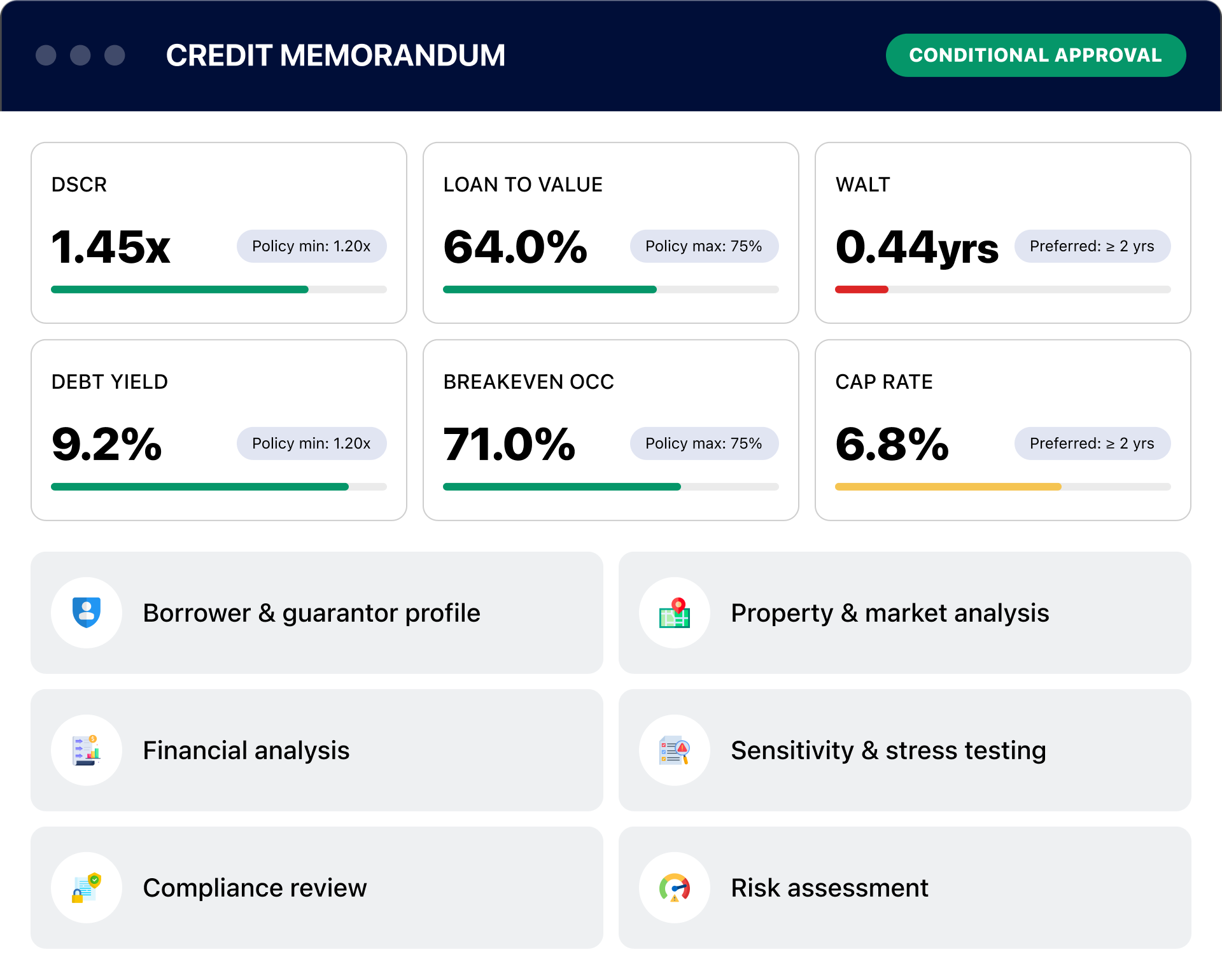

A CRE loan has five moments where things go wrong

We built around each one — not to replace your judgment, but to make sure you have the full picture at every stage.

A deal package arrives: appraisal, rent roll, operating statements, tax returns, personal financial. The information is all there. But extracting it takes days of manual work before any actual underwriting begins.

The problem: time lost before analysis startsNot all NOI is equal. One-time income, below-market rents, management fee exclusions, vacancy timing — a property can look profitable on paper and be structurally weak. This is where inconsistency between analysts creates the most risk.

We normalize consistently, with a full adjustment trailThe tenant mix determines whether that income is durable. One tenant at 50% of the rent roll with 14 months left on their lease is a fundamentally different risk than 10 tenants each at 10% on long-term leases. This distinction rarely gets surfaced clearly enough, fast enough.

Concentration and rollover exposure shown immediately from the rent rollFor owner-occupied deals, the business is the repayment source. For investment deals, the guarantor may be the backstop. Either way, the full picture requires connecting entities, personal finances, and contingent liabilities that rarely arrive in one place.

Global cash flow assembled across all uploaded entities and documentsA 5-year CRE loan that performs fine today can be a problem at maturity if the market has moved, the tenants have left, or rates have risen. Most banks don't calculate refinance risk at origination. They discover it at renewal.

Refi proceeds, maturity gap, and stressed DSCR calculated at originationWhat slows your team down on every deal

These aren't technology gaps. They're time gaps — hours your best underwriters spend on mechanical work instead of judgment calls.

Your analyst opens Excel, copies lease expiration dates, calculates rollover percentages, flags concentration. Every deal. Every time. One typo changes the risk picture entirely.

"By the time I finish spreading the rent roll, I've lost half a day on a deal that might not get approved."

Two underwriters on the same deal reach different normalized NOI figures. One adds back the management fee. One doesn't. Neither is wrong — but the inconsistency creates credit committee friction and audit exposure.

"We've had examiners ask why the same property was underwritten differently six months apart."

By the time a maturing loan can't refinance itself, you're in workout mode. The data to catch it early — NOI trend, cap rate movement, maturity balance — was always there. It just wasn't being connected.

"We knew the loan had a short fuse. We just didn't know until it went off."

The guarantor's other businesses, the related-party leases, the contingent liabilities — a lender needs all of it together to see true repayment strength. Instead it's assembled by hand, every deal, with no consistency check.

"Nobody has a complete picture until the credit memo is being written — and by then it's almost too late to change the structure."

The same work.

Done before you open Excel.

We don't change how you underwrite. We do the mechanical part before your team starts — so every hour is judgment, not data entry.

Every document your underwriters already collect

No new data. No new workflow. Upload what you have — we do the reading.

Your borrowers' data stays yours.

Before your compliance team approves any vendor touching borrower data, they need one question answered: where does this data go? Here is the plain answer — our certifications and our AI provider's certifications, in one place.